Back in June, we wrote a quick article outlining why we thought InMode Ltd., a medical aesthetic devices stock, was undervalued. Since then, the stock has returned about 50%. For a number of reasons, we still think INMD is a great stock to buy and has the potential have stellar returns going forwards. Keep reading to find out why. Summary:

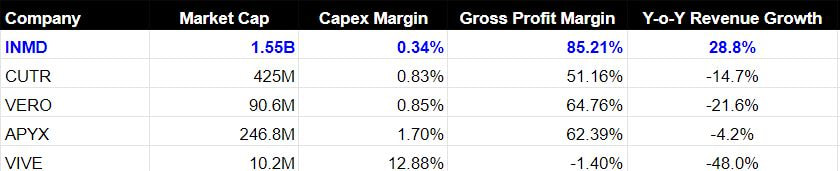

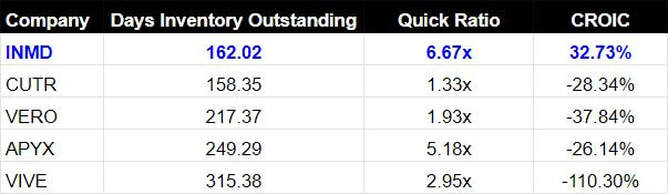

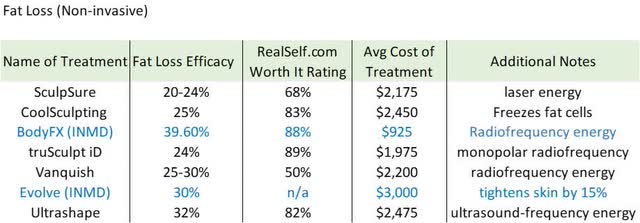

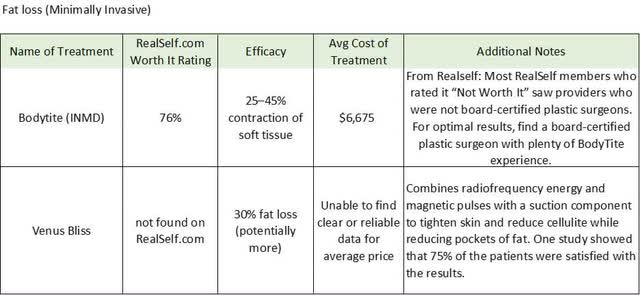

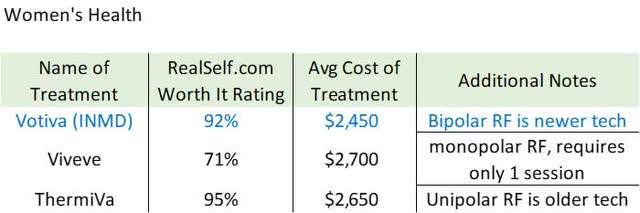

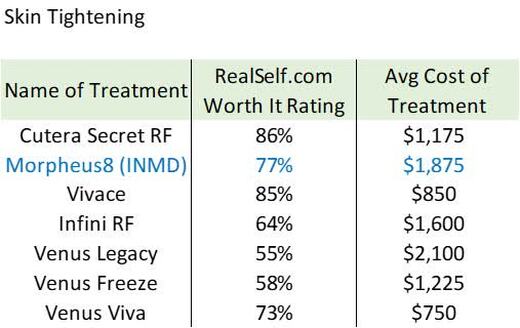

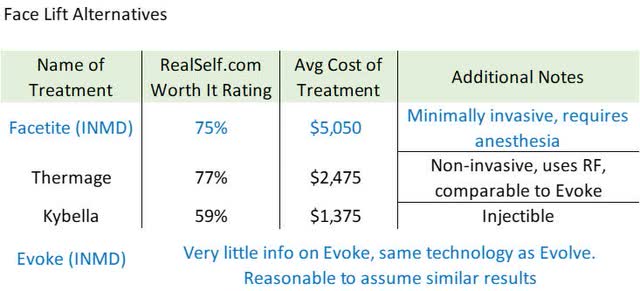

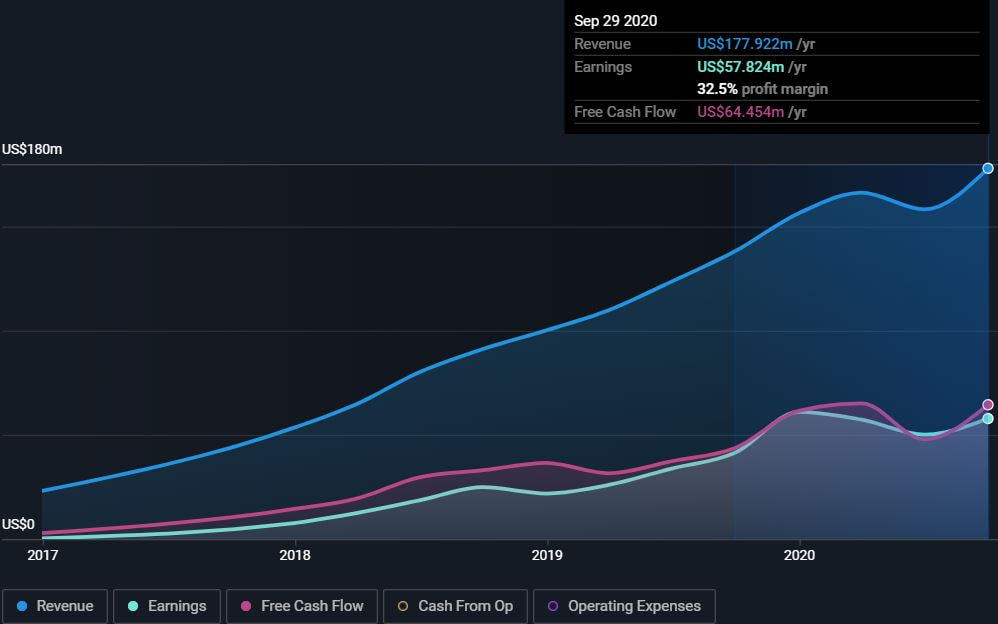

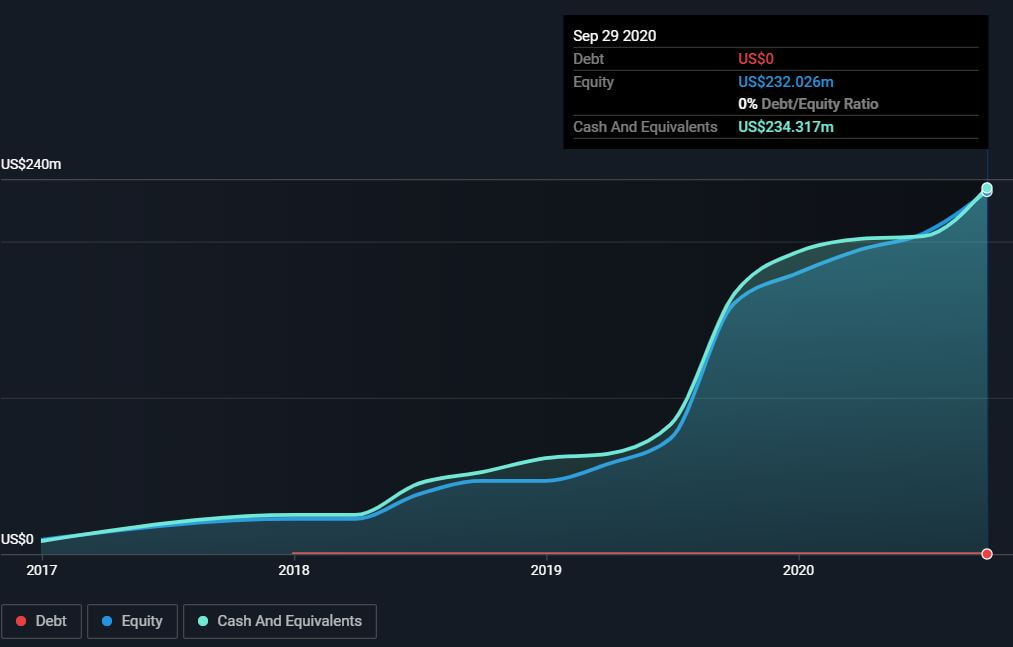

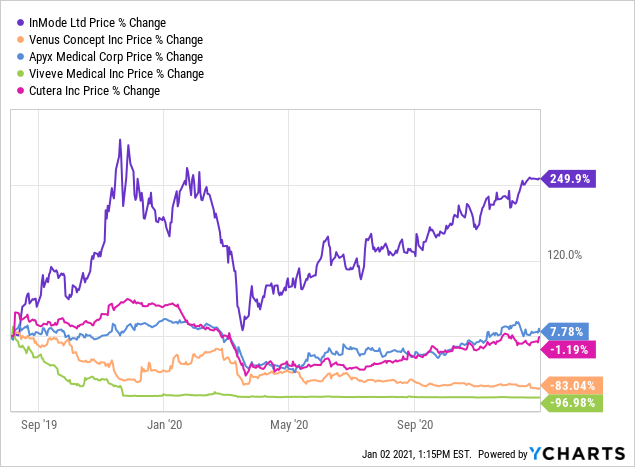

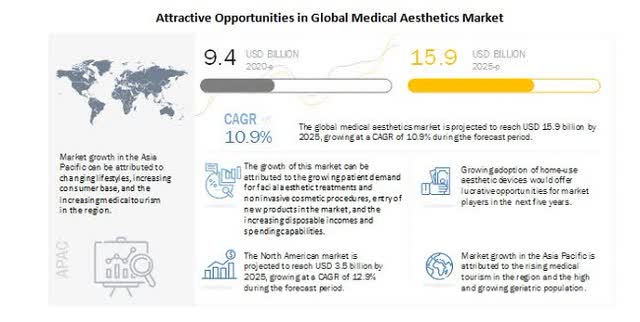

What is InMode About? InMode Ltd. (Ticker: INMD) is a provider of minimal and non-invasive radio-frequency technology. Its innovative technology strives to improve surgical procedures. These commercialized products are used by plastic surgeons, gynecologists, dermatologists, and more. Its products are made for a variety of purposes including liposuction, permanent hair reduction, facial skin rejuvenation, wrinkle reduction, cellulite treatment, skin appearance and texture, and superficial benign vascular and pigmented lesions. InMode operates in the United States and internationally. It was founded in 2008 and is headquartered in Yokneam, Israel. Why Is InMode A Good Buying Opportunity? InMode is the best stock in the quickly growing medical aesthetic devices industry, which is why it has outperformed its peers. It sports a high cash return on invested capital of 32%, consistently high gross margins, very low capital expenditures, high growth, and a flawless balance sheet with no debt. Although the company saw headwinds due to COVID-19 earlier in the year, by Q3, the demand for its products was pent-up which allowed INMD to make up for the temporary loss in sales. There is still ongoing demand according to management, during a time period where demand typically drops off. INMD is a founder-led company and its insiders own a large portion of the stock. These insiders haven't sold a share the entire year, implying that they believe in the company and are focused on long-term objectives. The products are also trusted by many celebrities such as Kim and Kourtney Kardashian. In addition, the company recently started a share buyback program (more on this below). We think this is a good use of their excess cash. A potential multi bagger: If you have read the book 100 baggers by Christopher Mayer, then you would realize INMD has many of the qualities of a multi bagger. These qualities include founder-operated businesses with high returns on capital, growth, high gross profit margins, share buybacks (when done right), potential for P/E expansion (INMD's P/E ratio is about 27, which is not high at all for a growth stock), and more. INMD's market cap is about $1.5B, or 3x larger than the average 100 bagger of $500M market cap. Therefore, we are not expecting a 100x return on the stock any time soon, but it definitely has the potential for an excellent return. Here's an article that outlines most of the lessons (but not all) that you can learn from 100 baggers. Lastly, based on our conservative estimates, INMD is trading near fair value. Great companies trading near or under fair value warrant a buy rating from us. How Has The Company Performed Throughout COVID-19? 2020 was a crazy year, but here's how InMode dealt with it: In Q2, INMD saw a 21% drop in revenue year-over-year. This should come as no surprise though. The great thing about its Q2 performance is the fact that it held up so much better than its competitors and still remained profitable (more detailed competitor analysis below). At a time when competitors were downsizing their operations, InMode thought it was best to keep investing in their business as usual, according to CEO Moshe Mizrahy. This strategy ended up working. In Q3, INMD saw record revenue, a 49% increase year-over-year, which brought record earnings and cash flow along with it. The strong results lead INMD to start a 1 million share buyback program in Q3. When asked by an analyst if there would be even more buybacks in the future, CEO Moshe Mizrahy said "later on maybe we'll add more". The company has lots of cash to deploy and a perfect balance sheet, but it is being careful and strategic with its capital allocation. InMode has also seen a lot of demand for its products since Q3. In the Q3 conference call, Spero Theodorou of InMode said: "So, we're actually seeing a lot of demand. We thought the demand initially was compressed demand for back in the spring and we kind of expected it to sort of taper off in the months of September, October. But these are unusual times and demand has continued. And exactly like Shak said, it's not necessarily everywhere the same, but the continued demand is an aberration because traditionally, in the aesthetic world, usually, September things typically drop off from the more plastic surgery procedures and the mothers usually take the kids back to school. It's a large element of the practices. But we haven't seen that. This is continuing demand. I think it's because of people having what Shak said, definitely have more income and sitting around and not spending on other things, but we've continued to see this demand through this period of time, which is definitely unprecedented. And we welcome it, of course." Overall, INMD is doing quite well now, and the operating results prove it. How Does InMode Compare To Its Peers? Below is an industry analysis comparing INMD to its direct competitors that are publicly traded. We broke it up into 2 images just so it's larger/easier to read.   Image source: StockBros Research, using data from Finbox Capital Expenditures Margin: INMD has very low capital expenditures (0.34% of total revenue). This means that it does not need to reinvest much into the business to grow, leaving it with strong amounts of free cash flow. Most of the other competitors have low capex margins as well, but INMD leads in this. Gross Profit Margin: InMode has the highest gross profit margin (85.2%) by a large margin, no pun intended. (VERO) is the closest competitor at around a 65% gross profit margin. Y-o-Y Revenue Growth: While the competitors have seen revenue declines this year because of COVID-19, INMD was still able to achieve 28.8% revenue growth compared to its last twelve months. This is very impressive given the circumstances. Days Inventory Outstanding: This is essentially the amount of days it takes for a company to sell its inventory. INMD and CUTR lead this one, with CUTR being slightly better at 158 days (the lower the better), but the other competitors are not even close. Quick Ratio: A measure of a company's liquidity (the higher the better). INMD leads this category as well at a 6.7x quick ratio. Cash Return on Invested Capital: InMode is the only free cash flow positive (and net income positive) stock in the competitors list. Therefore, it is the only one with a positive CROIC. CROIC is calculated by taking free cash flow and dividing it by the average invested capital. There are a few ways of calculating invested capital, but for this comparison we applied the conservative method of using average debt + average equity. Using this method, INMD's CROIC was still ~33%, which is again very impressive given the pandemic. Comparison of Industry Procedures We have compiled a list of different procedures that compete with InMode a grouped them in the following categories: Fat Loss (Non-invasive), Fat Loss (Minimally Invasive), Women's Health, Skin Tightening, and Face Lift Alternatives. We compare the average costs and worth it ratings obtained from realself.com. RealSelf is a very popular website for cosmetic surgery/procedures reviews. This includes reviews by both doctors and patients.      Source for all 5 images: StockBros Research As you can see, InMode's products are very competitive, especially with its fat loss technology. The company has a good mix of products that deliver great results at better prices as well as products that command a premium over comparable ones. Past Performance One thing that stands out when looking at INMD is its very high gross profit margins (see below).  Source: Finbox The company has been able to maintain gross margins above 80% since 2017, indicating that it has been able to defend itself against competition (a competitive disadvantage would cause INMD to see declining margins over time). Even during the worst of the pandemic in Q2, it was able to maintain its gross profit margins. Consistent Growth: Below is a chart showing revenue in blue, earnings in green, and free cash flow in purple. Except for the Q2 COVID-19 drag on operations, INMD has consistently grown every quarter. Its growth is attributed to investing in research & development to create great products and a successful sales and marketing team to bring awareness to consumers.  Source: Simplywall.st Strong Balance Sheet: INMD has a perfect balance sheet with no debt and $234 million in cash & equivalents, shown below.  Furthermore, InMode is highly liquid, with a current ratio of 7.2x and a quick ratio of 6.7x. It also has low inventory requirements. Its current inventory is only worth about $14.87 million. Strong Fundamentals Allowed INMD's Stock To Outperform Peers: Below is a chart of INMD's stock price % change since its IPO in 2019. As you can see, it vastly outperformed its peers.  INMD also outperforms on a 1-year chart, as it has returned over 21% in the past year while all the competitors are negative in the same period. Celebrities Love InMode ProductsMarketing is obviously very important. InMode has done a great job using Paula Abdul as its brand ambassador. Other celebrities like Kim and Kourtney Kardashian, Amber Rose, Noah Cyrus, Paige Hathaway (and many others) have used its products. InMode is a well-known company in the industry with a great product that even celebrities trust, so this gives us more confidence in its products. Here's a snippet from InMode's website:  InMode makes sure to market the fact that their products are minimally invasive, which is a key selling point since no one wants to experience scarring after a procedure. Industry Forecasts According to marketsandmarkets.com, the global medical aesthetics market is projected to reach USD 15.9 billion by 2025 from USD 9.4 billion in 2020, at a CAGR of 10.9%. This is due to a growth in popularity for minimally invasive and noninvasive aesthetic procedures, further innovation of these medical devices, and an increasing demand for aesthetic treatments among men. Here's one thing to keep in mind though: Market growth is limited to a certain extent by factors such as the clinical risks and complications associated with these types of procedures and the increasing availability of alternative beauty and cosmetic products.  Source: marketsandmarkets.com INMD's market cap is about $1.5B. With the global medical aesthetics market forecasted to be worth $15.9B by 2025, there is still room for the company to grow in its industry. Insiders Own A Large Portion of The Company Another thing that makes us confident with InMode is the amount of stock that insiders own, particularly the first 4 in the image below.  Source: Simplywall.st Let's start with the first two from the picture: Michael Kreindel (Chief Technology Officer and Director), and Moshe Mizrahy (Chief Executive Officer and Chairman of Board of Directors). Both of them co-founded InMode in 2008 and own a combined ~29% stake of the company. They were also both co-founders of Syneron Medical Ltd., another medical devices company, and were there from 2001-2007. So, this isn't their first rodeo, they have experience. Then, there is Israel Healthcare Ventures as the 3rd largest holder. It was founded and has been managed by Dr. Hadar Ron, who is part of the board of directors. So, adding those 3 board of directors gets you to about ~42% ownership, which is impressive. The next one, Stephen Mulholland Family Trust, is also interesting. Dr. Stephen Mulholland is not part of the board of directors, but he is a well-known Canadian plastic surgeon (and former hockey player). The fact that people who are specialized in the industry are heavily invested in INMD gives us extra conviction that the company is solid. What Is The Importance Of All This? The main reason that this is important is because founder-led companies usually outperform the market. This is a well-known fact, but if you don't want to take our word for it, check out this article from Harvard Business Review. This was also discussed in the book 100 Baggers by Christopher Mayer that we mentioned earlier. Some great examples of this are (FB) and (AMZN). So, this applies to the top 2 holders of INMD. The article goes into more detail, but here's the main idea: "Founders have the moral authority to make the hard choices, they know the detail of the business and have better instincts, and they have a long-term perspective on investments and building a company that lasts." It also states that founder-led companies are more innovative and quicker to act. This is exactly what makes INMD so good. Their co-founders know the business in and out, and built it themselves. If a company doesn't innovate, especially in the tech industry, it's most likely going to fail. Next, Dr. Hadar Ron is a medical specialist with lots of business experience, being involved with around a dozen other businesses. Therefore, she seems fit for her role as a board member of INMD with 13% ownership. Lastly, with Dr. Stephen Mulholland, as we mentioned earlier, we think a large position from a well-known plastic surgeon is a great sign. What we like about this ownership composition (especially the co-founders), is that these types of shareholders generally don't sell often. They want to see the business grow, and because they have a large investment and interest in the business, they will make sure that happens. Insiders haven't sold at all in the past 12 months, even though the lock-up period expired in early February. See below:  Source: Simplywall.st This reinforces our point that it's unlikely for these kinds of owners to sell. No one has bought either, but we are not concerned about that since the ownership is already so high. ValuationBased on our estimates, InMode is valued between $45.92 (fully diluted) - $52.66 (basic shares). However, we would strongly like to stress the fact that this is our base case conservative estimate which assumes revenue will continue to grow at $50 million for the next 6 years. Given that the company has very strong cash flows, and industry consolidation has become more common, it is reasonable to assume that InMode will participate in mergers and acquisitions. In addition, it's also reasonable to assume that the company will continue to make great technological discoveries as its cash flows and cash position continues to grow. We believe that these 2 factors will result in higher future cash flows than our forecast. Furthermore, management expects taxes in 2021 to remain the same and then increase to 11-12% in 2022. We assumed a tax rate of 11.5% until 2025 and then increased to 17% for the stable phase (marginal tax rate of InMode as per Finbox).  Source: Author |

|  |

Categories

All

Educational

Learn Fundamental Analysis

Learn Technical Analysis

Research Reports

Stock Market Books

Stocks To Watch

Archives

September 2022

April 2022

March 2022

February 2022

January 2022

December 2021

November 2021

October 2021

September 2021

August 2021

July 2021

June 2021

May 2021

April 2021

March 2021

February 2021

January 2021

December 2020

November 2020

October 2020

September 2020

August 2020

July 2020

June 2020

May 2020

March 2020

December 2019

August 2019

July 2019

April 2019

RSS Feed

RSS Feed